The Economic Impact of the Health and Wellness Industry: A Comprehensive Analysis

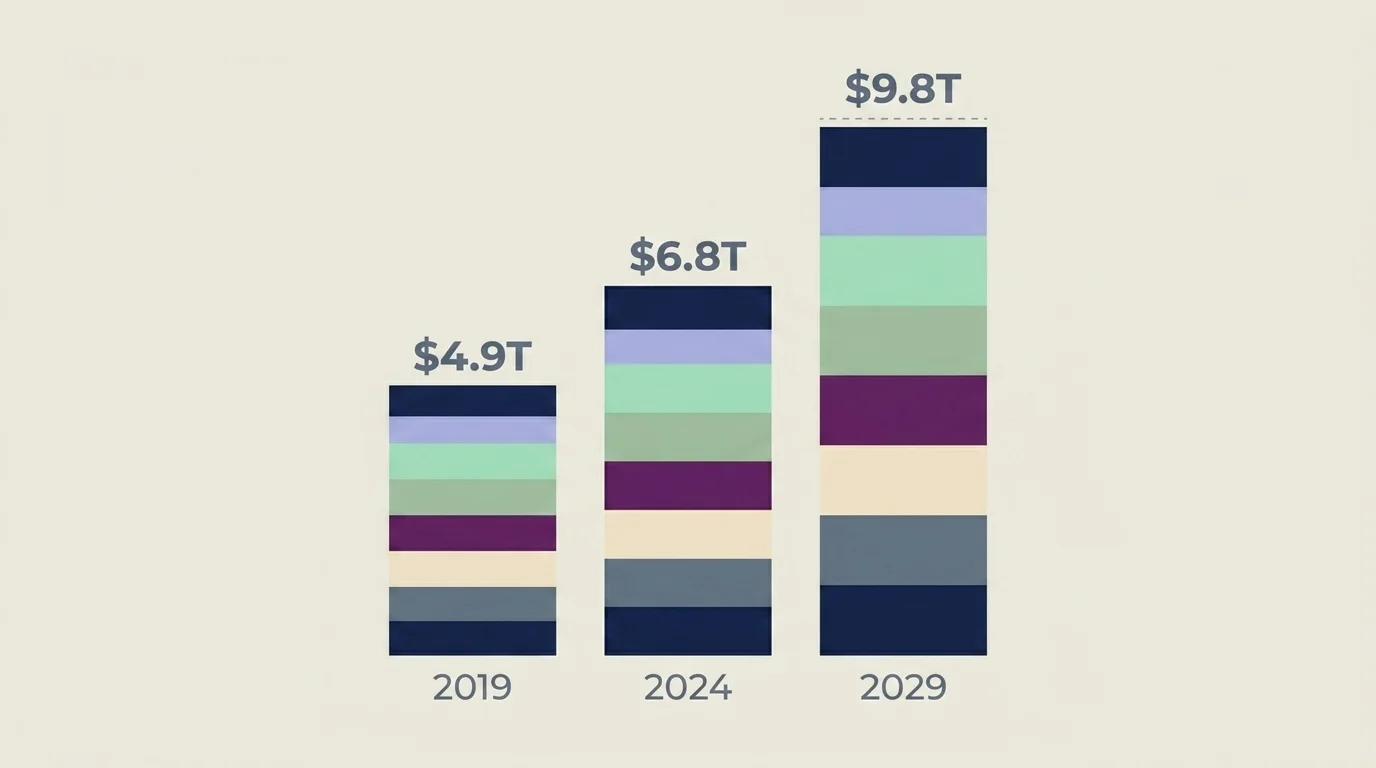

I want to start with a number, because everyone writing about the health and wellness industry should. The Global Wellness Institute's 2025 Monitor, released in November 2025, puts the global wellness economy at $6.8 trillion in 2024 — up 7.9 percent from the year before, and forecast to reach $9.8 trillion by 2029 at a 7.6 percent compound annual rate (Global Wellness Institute). That is the headline. Most articles you will find on this topic still quote the $5.6 or $6.3 trillion figures from 2022–2023 monitors. They are out of date.

I am a clinician, not an industry analyst. What I want to do here is take the figures the GWI and McKinsey have put on the table, lay them out in a way that does not require a finance background to read, and be honest about the parts I find clinically interesting — including the parts I find clinically uncomfortable. The wellness industry is a category that includes the meditation app that helps a client manage panic, and it also includes a great deal of marketing aimed at people whose actual need is therapy. Both are inside the $6.8T number.

What is the wellness industry?

It is a category, not a sector, and that is part of what makes it confusing. The Global Wellness Institute — which is the body whose figures every other research firm cites, so we may as well use their definition — sorts the wellness economy into eleven sectors:

- Personal Care & Beauty

- Healthy Eating, Nutrition & Weight Loss

- Physical Activity

- Wellness Tourism

- Public Health, Prevention & Personalized Medicine

- Traditional & Complementary Medicine

- Wellness Real Estate

- Mental Wellness

- Spas

- Thermal & Mineral Springs

- Workplace Wellness

Three of these — personal care and beauty, healthy eating, and physical activity — account for roughly 53 percent of the total (GWI 2025 Monitor). Mental wellness, the sector I work adjacent to, is one of the smaller ones by absolute size, though it is among the fastest-growing.

The category includes both clinical and non-clinical activity. A licensed therapist's session and a drugstore essential-oil diffuser both count, which tells you something important about what this number is and is not. It is a measure of consumer spending on goods and services framed as wellness, not a measure of how much population health has improved.

How big is the wellness industry, really?

In 2024 the wellness economy reached $6.8 trillion, equal to about 6.12 percent of global GDP (GWI Statistics & Facts). For scale, that is larger than the GDP of every country on earth except the United States and China.

The growth rate matters as much as the absolute size. From 2013 to 2024, the wellness economy grew at roughly 6.5 percent per year, against global GDP growth of about 3.2 percent in the same period (GWI 2025 Monitor). That is more than double-paced expansion sustained over a decade. The pandemic suppressed wellness spending briefly in 2020–2021; the recovery and re-acceleration since 2022 has been faster than the historical trend, which is why the 2029 forecast ($9.8T at 7.6 percent CAGR) is now higher than the prior decade's actual run rate.

A second analyst, Towards Healthcare, runs a parallel sizing for the broader health-and-wellness market — $6.16T base in 2025 growing to $10.48T by 2035 at a 5.46 percent CAGR (Towards Healthcare). Sanity check: their figure and GWI's are within methodological distance of each other, with the differences explained by sector inclusion. When two independent sources agree on the order of magnitude, the headline is solid.

The eleven sectors, sized and sorted

The most useful way to read the wellness economy is to break it down by sector. The numbers below come from the Global Wellness Institute's 2025 Monitor and its press materials.

| Sector | 2024 size / signal | 2019–2024 CAGR | What it includes |

|---|---|---|---|

| Personal Care & Beauty | Largest single sector by spend | Moderate | Skincare, cosmetics, beauty-as-wellness retail |

| Healthy Eating, Nutrition & Weight Loss | Top-3 sector | Moderate | Functional foods, supplements, weight-management programs |

| Physical Activity | Top-3 sector | Moderate | Gyms, classes, fitness tech (~$86B sub-segment) |

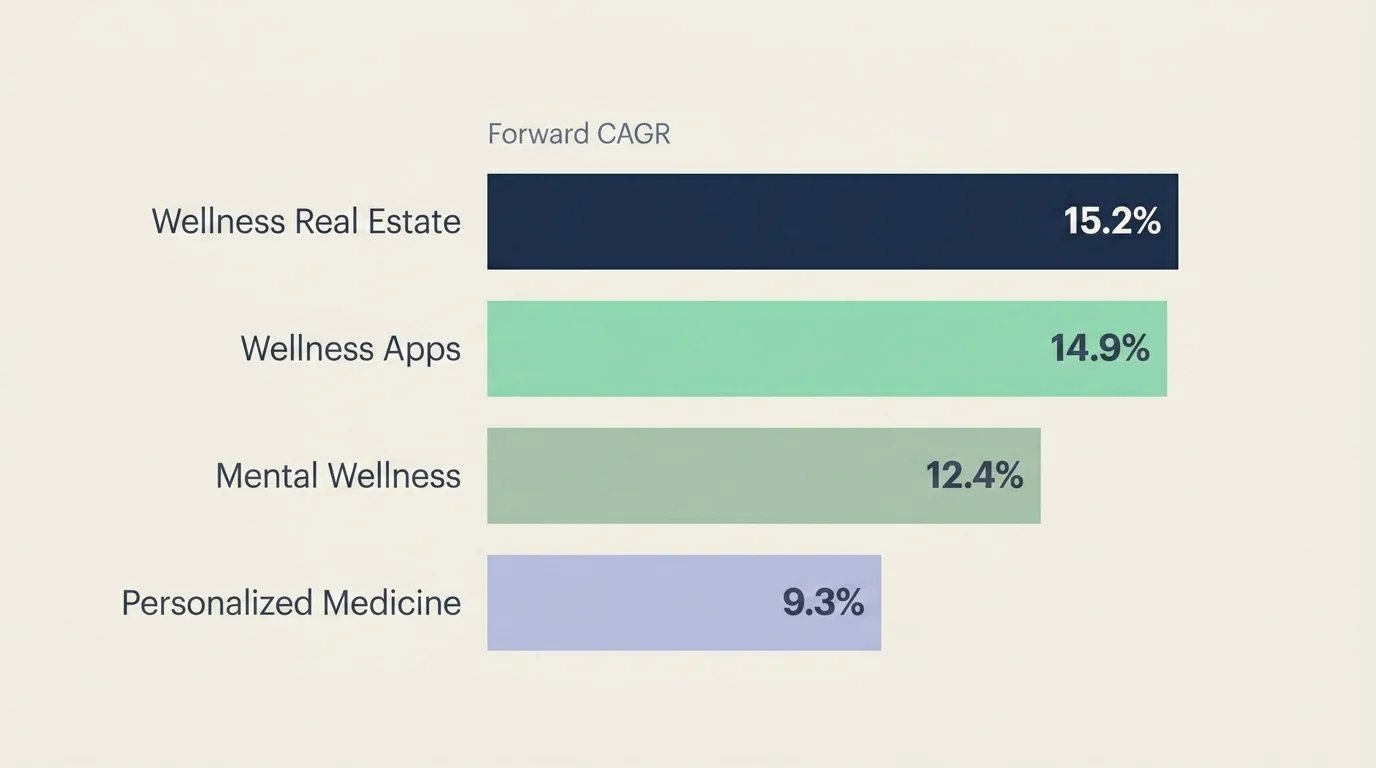

| Wellness Real Estate | Fastest 5-yr growth | 19.5% | Wellness-oriented residential, communities, hospitality builds |

| Mental Wellness | Among fastest | 12.4% | Apps, therapy access, meditation/mindfulness platforms |

| Wellness Tourism | Strong post-pandemic rebound (+13.8% '23–4) | High | Spa retreats, wellness-led travel |

| Spas | +14.6% YoY 2023–4 | Recovering | Day spas, hotel spas |

| Thermal & Mineral Springs | +11.1% YoY 2023–4 | Recovering | Natural-springs hospitality |

| Public Health, Prevention & Personalized Medicine | Personalized medicine $147B sub-segment | 9.3% (forward) | Genomics-led prevention, screening, personalized therapeutics |

| Traditional & Complementary Medicine | Moderate | Stable | TCM, Ayurveda, herbal medicine |

| Workplace Wellness | -1.5% YoY 2023–4 (only shrinking) | Low | Corporate programs (sub-segment $55.1B → $70.1B 2025–2033 per Grand View Research) |

Sources: GWI Nov 2025 release, GWI Nov 2025 blog, Athletech, Grand View Research — Corporate Wellness.

A few sub-segments worth pulling out, because they are growing inside their parent sectors at rates that change the picture. Cannabis-as-wellness is at a 26 percent five-year CAGR, meditation and mindfulness at 18.9 percent, sleep at 12.6 percent (ATFW summary of GWI 2025). Wellness apps as a stand-alone digital category are forecast to reach $26.19 billion by 2030 at a 14.9 percent CAGR (Grand View Research).

A note on the one sector that is shrinking

I am going to spend a moment on workplace wellness because it is the most clinically interesting line in the table. According to GWI, workplace wellness spending contracted 1.5 percent from 2023 to 2024 — the only sector in the eleven to shrink. Grand View Research projects the corporate sub-segment will still grow, but at a 3.1 percent rate, well below every other sector. My read, from inside clinical practice, is that the contraction reflects a long-overdue reckoning: employers are pulling back from generic step-counter programs and meditation apps that produced negligible measurable improvements, and a meaningful share of that spend is migrating to therapy benefits and EAP programs that are not always counted inside the wellness category. If you read the workplace-wellness shrinkage as a sign the industry is failing, you are reading it backwards. What is failing is one specific kind of corporate wellness theater.

Wellness vs the pharmaceutical industry

This is the comparison no one in finance media is making cleanly, and I want to spend a section on it because it is structurally important.

The global pharmaceutical industry is roughly $1.8 trillion. The wellness economy is $6.8 trillion. The wellness economy is therefore about four times the size of pharma, and it accounts for 60 percent of global health expenditures, which the GWI puts at $11.2 trillion overall (GWI Nov 2025 blog).

What does that 4x gap mean? Not what an investor reflexively wants it to mean. The wellness economy and the pharmaceutical industry are not selling competing products to the same buyer. Pharma is overwhelmingly reimbursed through insurance and government payers, with clinical trials, regulatory approval, and a buyer at the back end (the prescriber) who is professionally accountable for the choice. Wellness is overwhelmingly self-pay, lightly regulated, and the buyer is the end user — usually unmediated. The two industries are operating in different markets with different feedback loops on whether a product actually works.

That difference is what makes the next number — the clinical-over-clean shift — so significant.

Health and wellness trends 2026

McKinsey's Future of Wellness consumer survey for 2024–2025 reports a meaningful change in how Western consumers are choosing wellness products. About half of US and UK consumers now cite clinical effectiveness as a top purchasing factor, and doctor recommendations are gaining trust over influencer endorsements (McKinsey). This is a reversal of the "clean / natural / plant-based" framing that dominated wellness marketing from roughly 2018 to 2022.

Why this matters clinically: when consumers ask "does this work" before "is this natural", the products that survive the question change. Evidence-based offerings — therapy access, validated sleep interventions, peer-reviewed supplement formulations — have an opening they did not have five years ago. So do scams that learn to use the word "clinical" without actually meaning it. The selection pressure has shifted but the discernment burden on consumers has not gone away.

A second trend, also from McKinsey: Gen Z and millennials are 36 percent of US adults but drive about 41 percent of annual wellness spending, and roughly two-thirds of them bought functional-nutrition products in the past year across the US, UK, and Germany. Younger consumers are over-indexed on this category and they are concentrating spend in functional categories (sleep, focus, hormonal health, gut, mood) rather than aspirational ones (yoga retreats, luxury spa).

The third 2026 trend worth surfacing — and the one closest to my clinical practice — is the continued growth of mental wellness as a distinct sub-category at 12.4 percent five-year CAGR. The category includes therapy-access apps (BetterHelp, Talkspace, regional equivalents), meditation platforms (Calm, Headspace), and a fast-growing tier of AI companion apps that I have professional reservations about but cannot ignore as a market force.

Where the growth lives — for the people thinking about money

I am not a financial advisor, and I am going to keep this brief because the responsible answer for retail investors is to ask one. But the data does tell you where the wellness category is putting its growth, and that is useful context even if you never buy a share of anything.

The highest sustained growth rates among major wellness sub-segments, ranked by forward CAGR:

- Wellness Real Estate: 15.2 percent projected annual growth 2024–2029 (GWI)

- Wellness Apps: 14.9 percent CAGR to $26.19B by 2030 (Grand View Research)

- Mental Wellness: 12.4 percent five-year (2019–2024) historical CAGR (GWI)

- Personalized Medicine: 9.3 percent CAGR forward, $147B current size (GWI)

What this signals: the growth is in physical infrastructure (real estate built around wellness amenities), in software (apps), and in clinically grounded categories (personalized medicine, mental health platforms). It is not in the spa-and-retreat tier. The category is professionalizing.

Forecast to 2029: $9.8 trillion and what it relies on

The GWI projects the wellness economy at $9.8 trillion by 2029, at a 7.6 percent compound annual growth rate (GWI Nov 2025 release). That projection rests on three load-bearing assumptions worth naming honestly.

The first is that wellness real estate continues to grow at 15.2 percent forward — a rate that depends on residential and hospitality developers continuing to embed wellness amenities at premium price points. If consumer real-purchasing-power softens, this is the sector most exposed to revision.

The second is that mental wellness sustains its 12-percent-range growth. This depends partly on insurance and partly on the willingness of consumers to keep paying out of pocket for therapy access, app subscriptions, and adjacent services. It is the sector with the most clinical legitimacy and also the most subscription fatigue risk.

The third is that the clinical-over-clean consumer shift continues to drive functional-nutrition and personalized-medicine spending among younger consumers. This is the assumption I find most credible, because it is downstream of a change in consumer judgment that does not appear to be reversing.

A regional read

GWI flags the Americas, MENA, and Europe as the strongest five-year regional performers (GWI Statistics & Facts). Asia-Pacific contributes a structurally large share of the category, particularly in personal care, traditional medicine, and wellness tourism, and remains a growth driver from a larger base. The North American share is still the largest by absolute spend; Europe is closing the per-capita gap. For most readers, the actionable read is that this is a globally distributed category, not a US-centric one, and the regional growth rates are converging more than diverging.

A clinician's honest read

Here is what I find clinically useful about the $6.8 trillion figure, and what I find clinically uncomfortable about it.

What is useful is that the headline number forces honesty about a category that has been treated, by both critics and boosters, as a soft, mood-based thing. It is not. It is roughly four times the size of the pharmaceutical industry and growing twice as fast as global GDP. Whatever one thinks of essential oils or step counters or sound baths, this category is now a structural feature of the global economy, and dismissing it does not make it smaller. It is shaping how working-age adults spend their discretionary money on their bodies and their minds.

What is uncomfortable is that the same number does not tell us whether any of that spending is producing better mental or physical health for the people doing the spending. The clinical-over-clean shift in McKinsey's data is a real and welcome signal — consumers are starting to ask the right question. But the wellness industry is not the same thing as the public-health system, and a 7.6 percent CAGR is not a measure of population well-being. Mental wellness as a sector is growing at 12.4 percent annually, and yet anxiety, depression, and loneliness in the US are not in retreat. The category is selling something. Whether the something is what people actually need is, in many cases, an open clinical question.

If you are a reader using this article to make a financial or career decision, the data is solid and the trajectory is up. If you are a reader using this article to make a personal wellness decision, the more useful frame is the one McKinsey's own data points at: ask whether the thing you are about to buy has actual evidence behind it. And remember that therapy is not a luxury. If you are in crisis, in the United States, please call or text 988.

Frequently Asked Questions

The Global Wellness Institute's 2025 Monitor pegs the global wellness economy at $6.8 trillion in 2024, up 7.9% from 2023. It is forecast to reach $9.8 trillion by 2029, growing at a 7.6% annual rate — more than double the pace of global GDP growth over the same period.

Yes. The wellness economy ($6.8T in 2024) is roughly four times the size of the global pharmaceutical industry ($1.8T) and accounts for 60% of total global health expenditures ($11.2T). The two industries operate in different markets, however — pharma is largely insurance-reimbursed and clinically regulated; wellness is largely self-pay and lightly regulated.

The Global Wellness Institute tracks 11 sectors: Personal Care & Beauty; Healthy Eating, Nutrition & Weight Loss; Physical Activity; Wellness Tourism; Public Health, Prevention & Personalized Medicine; Traditional & Complementary Medicine; Wellness Real Estate; Mental Wellness; Spas; Thermal & Mineral Springs; and Workplace Wellness. The top three (personal care, healthy eating, physical activity) account for roughly 53% of the total.

Wellness Real Estate led the past five years at 19.5% annual growth, followed by Mental Wellness at 12.4%. Sub-segments showing the steepest CAGR include cannabis (26%), meditation and mindfulness (18.9%), and sleep (12.6%). Wellness apps as a stand-alone digital category are projected at 14.9% CAGR to $26.19B by 2030.

Three shifts are reshaping the category. First, consumers are pivoting from 'clean / natural' to clinically proven — about half of US and UK shoppers cite clinical effectiveness as a top purchase factor (McKinsey 2024). Second, doctor recommendations are gaining trust over influencer endorsements. Third, Gen Z and millennials — 36% of US adults — drive 41% of wellness spending, concentrated in functional-nutrition and digital mental wellness.

Yes — workplace wellness spending contracted 1.5% from 2023 to 2024, the only sector among GWI's eleven to decline. The likely driver is employers pulling back from generic step-counter and meditation-app programs that produced negligible measurable improvements, with a meaningful share of that spend migrating to therapy benefits and EAP programs.

Three structural drivers: a sustained consumer shift toward proactive and preventive health management; the professionalization of categories that were previously informal (mental wellness apps, personalized medicine, functional nutrition); and demographic concentration of spending among Gen Z and millennials, who are over-indexed on this category. The combined effect produced 6.5% annual growth from 2013 to 2024, against 3.2% global GDP growth in the same period.

Most credibly by following the growth-rate data rather than the marketing. The forward-CAGR leaders are wellness real estate (15.2%), wellness apps (14.9%), mental wellness (12.4% historical), and personalized medicine (9.3%). Investors should also weight clinical legitimacy heavily — the McKinsey clinical-over-clean consumer shift means evidence-based offerings now have a structural tailwind. None of this is financial advice; consult a licensed advisor for portfolio decisions.

Check Out These Related Articles

Financial Fitness: Exploring the Intersection of Wealth and Well-Being

Emotional Well-Being: Consumer Priorities and Influential Factors

The Economics of Integrative Medicine: Balancing Health Outcomes with Financial Considerations