The Business of Well-Being: Exploring Financial Considerations in Holistic Health

In Waimānalo, on the windward side of O'ahu, a lomilomi practitioner is teaching a small class. Down the road, a resort spa is selling a forty-five-minute "lomilomi-inspired" treatment at a premium price point. Both transactions are inside the same wellness business, which the Global Wellness Institute now sizes at $6.8 trillion globally in 2024, with a forecast of $9.8 trillion by 2029 at a 7.6 percent compound annual rate (Global Wellness Institute, 2025 Monitor). One transaction is the transmission of a practice; the other is the consumption of a brand. They are not the same thing, and what I want to do in this piece is treat the industry seriously enough to say so while still naming the operator-level economics — the numbers, the margins, the regulatory channels — that any honest writer about the wellness business has to put on the page.

This is a guide to seven wellness business models in 2026. Each one comes with current segment sizing from GWI, indicative startup-cost ranges from operator-focused sources, and a brief anthropological note on what the segment actually is when you look closely at it.

How big the wellness market actually is

The figure to anchor everything else to is $6.8 trillion. That is roughly 6.1 percent of global GDP, growing at 6.5 percent annually since 2013 against global GDP growth of 3.2 percent in the same period (GWI 2025 Monitor). The category has been compounding at roughly double the broader economy for a decade.

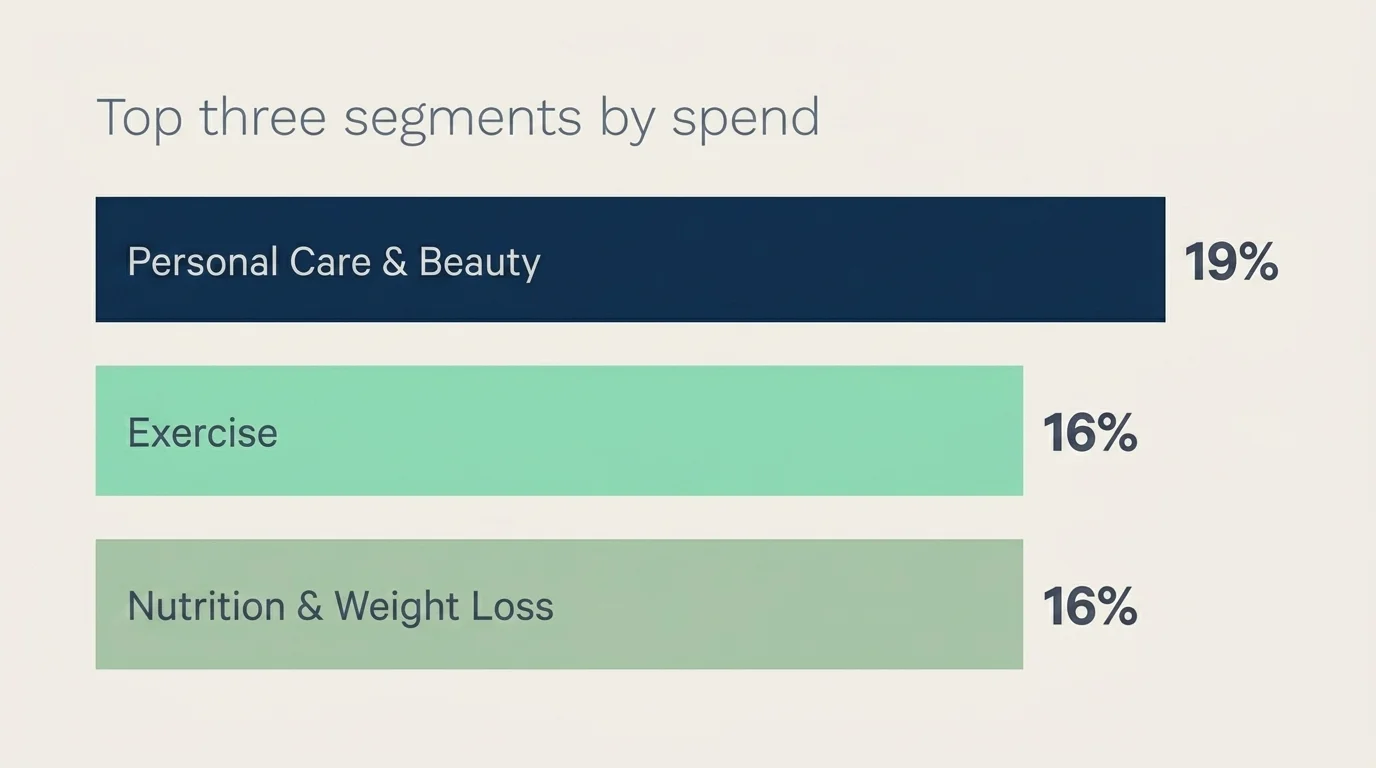

Three sub-segments dominate the revenue split. By 2025 share figures, personal care and beauty account for 19 percent of wellness spend, exercise 16 percent, and nutrition and weight loss 16 percent (Wellness Creative Co.). Combined, those three categories carry just over half of the $6.8T total. The remainder is distributed across mental wellness, wellness real estate, wellness tourism, spas, traditional medicine, public health and preventive medicine, thermal/mineral springs, and workplace wellness.

Per-capita spending is heavily regional. The average North American spends roughly $6,029 per year on wellness; the average European spends about $1,876 (GWI 2025). For an operator considering market entry, that gap is the most important number on this page — it tells you where price tolerance is, where it is not, and what kind of pricing models translate across geographies.

A second analyst, Precedence Research, runs a parallel sizing for the broader health-and-wellness market: $4.79T in 2025 growing to $7.76T by 2035 at a 4.94 percent CAGR (Precedence Research). Their inclusion criteria differ from GWI's, but the order of magnitude agrees, which is the test I care about when two independent sources are quoted in the same article.

1. Mindfulness and meditation as a business

The meditation-app category is where the post-pandemic wellness story turned. Calm's in-app revenue in January 2024 was approximately $7.7 million per month; Headspace's was approximately $4 million (appinventiv 2025) — substantial numbers. But the same source reports downloads declined 61 percent for Calm and 74 percent for Headspace between 2018 and 2024. The consumer-app era of the segment is mature. Headspace's October 2023 merger with Ginger to add clinical coaching and therapy reads, in retrospect, as the inflection point: the path forward for the segment is convergence with clinical and employer-paid channels, not a fourteenth meditation app.

Operator card — Mindfulness and meditation

- Segment size: meditation-management apps $2.20B-$8.87B in 2025 depending on scope (Grand View Research)

- Revenue model: subscription apps; corporate B2B licensing; live workshops; certified instructor services

- Startup cost: digital model $100-$2,000; a credentialed instructor service practice $500-$5,000 (Pure Green Franchise, Shopify)

- Key risk: consumer DTC is saturated and contracting; corporate channels favor incumbents with clinical credentials

- Anthropological note: "mindfulness," as a billable consumer product, is a translation of insight-based Buddhist meditation traditions through Jon Kabat-Zinn's MBSR framework. The clinical evidence base lives in MBSR; the billable consumer product version often does not include the meditation teacher, only the audio.

2. Nutritional supplements and functional nutrition

The supplements segment is where wellness most clearly crosses into low-regulation commerce. Functional nutrition — supplements positioned for specific outcomes (sleep, mood, focus, gut health, hormonal balance) — has been the fastest-growing edge of the category for the past three years, propelled by Gen Z and millennial buyers who are now 41 percent of US wellness spending despite being 36 percent of US adults (McKinsey).

Operator card — Nutritional supplements

- Segment context: Nutrition and weight loss = 16% of the global wellness economy (~$1.1T at the $6.8T total)

- Revenue model: DTC e-commerce; subscription auto-replenish; wholesale into specialty retail; private-label manufacturing

- Startup cost: $3,000-$60,000+ for a product brand, depending on whether the operator is private-labeling existing formulations or developing custom ones (Pure Green Franchise)

- Gross margin: 50-70% achievable on dropshipped/private-label SKUs; 40-60% common after fulfillment and customer-acquisition costs (Shopify)

- Key risk: FDA does not pre-approve supplement claims; the McKinsey "clinical over clean" consumer shift means unsubstantiated claims face faster reputational consequences than they did in 2020

- Anthropological note: many functional-nutrition product positions ("adaptogenic," "ayurvedic," "TCM-inspired") are stripped translations of formulations that, in their source traditions, are prescribed within a diagnostic relationship. The capsule is real; the diagnostic context — which is half of what the tradition is — usually does not travel with it.

3. Fitness and physical activity

Physical activity is 16 percent of the wellness economy by spend, anchored by gym memberships, boutique studios, and an $86B fitness-technology sub-segment that includes wearables, connected hardware, and streaming platforms (GWI 2025 Monitor, Athletech). The boutique-studio era that peaked around 2018 has consolidated; the consumer-hardware era that peaked around 2021 has corrected; what remains is a steadier mid-cycle market with two clear winners — independent trainer-led services and corporate B2B fitness benefits.

Operator card — Fitness

- Segment size: $86B in fitness technology alone; physical activity broadly is ~$1.1T of the $6.8T total

- Revenue model: studio memberships; personal training ($75-$200/session, $300-$5,000+ packages); merchandise; wearable hardware; class licensing

- Startup cost: $500-$999 for certification; $20,000-$150,000 for a boutique studio build (Shopify, businessplansuite)

- Key risk: post-2021 consumer-hardware contraction; rent and instructor-retention pressure on boutique-studio economics

- Anthropological note: imported movement traditions (yoga, Pilates, capoeira, qi gong) circulate inside this segment under fitness-industry pricing and pacing. The originating communities sometimes participate in the economic upside; more often they do not. Where authority lives in a practice — who can teach whom what — is a question worth asking before naming a class after a tradition.

4. Mental health and mental wellness

Mental wellness is the segment that has structurally separated from the rest of the wellness category and behaves more like a clinical sub-industry than a lifestyle one. It reached $441B globally in 2024 (US $125B, China $16B), grew 12.4 percent annually from 2019 to 2024, and is forecast at 10.1 percent through 2029 (GWI 2025 Monitor). It is the second-fastest-growing major segment in the wellness economy behind wellness real estate.

Two demand signals are converging. On the consumer side, 76 percent of US workers report at least one mental health condition. On the buyer side, 86 percent of insurance brokers report clients increasing mental health investment in 2025 — the sixth consecutive year mental health led their priority list (WISe Wellness Guild). And the ROI math is strong: workplace mental-health spending returns approximately $4 in productivity and absenteeism savings for every $1 invested (faspsych 2025).

Operator card — Mental wellness

- Segment size: $441B in 2024; 10.1% projected CAGR through 2029

- Revenue model: licensed therapy practice; B2B EAP contracts; app subscriptions; group programs; insurance + self-pay hybrid

- Startup cost: $100-$2,000 for a solo licensed-practitioner digital practice; $20,000-$150,000 for a multi-clinician brick-and-mortar group

- Reimbursement note: therapy and counseling services from licensed clinicians are widely covered by insurance, HSA, and FSA — see HSA/FSA section below

- Key risk: clinician licensing is per-state; cross-state telehealth complicates scale; over-reliance on consumer-pay can mask demand softness

- Anthropological note: "mental wellness" as a market category includes both clinical mental-health services (where there is a licensed provider and a measurable outcome) and AI companion apps and meditation platforms (where neither is necessarily true). The category's growth rate folds both together. Operators choosing where to position should know which side they are on.

5. Health coaching and wellness coaching

Health coaching sits in an interesting regulatory and economic position. It is unlicensed in most US states (the National Board for Health & Wellness Coaching offers a voluntary credential, not a license), which keeps the entry cost low and the credentialing market noisy. The economics work for a competent solo operator and are difficult at scale.

Operator card — Health and wellness coaching

- Revenue model: 1:1 coaching ($75-$200/session, $300-$5,000+ multi-session packages); group cohorts; corporate wellness contracts; online courses ($97-$997); memberships ($10-$250/month) (Shopify)

- Startup cost: $100-$2,000 (digital practice); $300-$5,000 for credentialing

- Key risk: market is crowded; corporate channels increasingly require board certification (NBHWC) to be on the panel

- Note on the SEO opportunity for operators reading this: "wellness coaching business" has a Keyword Difficulty of 2 — close to zero ranking competition for an operator who builds a credible content footprint

- Anthropological note: the modern coaching profession is a hybrid of Carl Rogers-style person-centered psychology, motivational-interviewing literature, and the management-consulting "executive coach" lineage. It is not the same thing as therapy, and a competent coach will say so before you ask.

6. Holistic healing modalities — acupuncture, naturopathy, traditional medicine

This is the segment closest to my fieldwork, and the one I want operators to read most carefully. The traditional and complementary medicine sub-segment of GWI's taxonomy includes acupuncture, traditional Chinese medicine, Ayurveda, naturopathy, herbal practice, energy healing, lomilomi, curanderismo, Kampo, and dozens of community-based traditions globally. The economics differ enormously between modalities that have established clinical licensure (acupuncture, chiropractic, naturopathic medicine in licensed states) and those that do not.

Operator card — Holistic healing modalities

- Revenue model: clinical practice with insurance/HSA-FSA reimbursement (where licensed); cash-based individual sessions; group workshops; product sales (herbs, supplements); educational programs

- Startup cost: $20,000-$150,000 for a clinical practice with treatment rooms; $1,000-$10,000 for a cash-based portable practice

- Reimbursement: significant — see HSA/FSA section

- Key risk: scope-of-practice regulation varies by state and country; misrepresenting traditional practice as biomedical treatment carries both ethical and legal exposure

- Anthropological note: the segment most prone to commodification. A licensed acupuncturist trained for three years in a TCM-accredited program and a weekend-certified "energy healer" both occupy this segment in market-research data. They are not the same thing, and prospective operators should be honest about which side of that line their practice sits on — and credit the lineage they are working within.

7. Wellness products and personalized wellness

The seventh category is the one that absorbs personalized medicine, wellness apps, sleep tech, and the broader "build a thing and sell it" wellness goods market. Personalized medicine alone is a $147B segment growing at 9.3 percent forward CAGR (GWI 2025). Wellness apps as a stand-alone digital category are projected at $26.19B by 2030 at 14.9 percent CAGR (Grand View Research).

Operator card — Wellness products and personalized wellness

- Revenue model: e-commerce DTC; subscription replenishment; affiliate commerce; B2B licensing

- Startup cost: $100-$2,000 for digital products (downloadables $10-$95, courses $97-$997); $3,000-$60,000 for physical products; $20,000+ for connected-hardware ventures

- Target margin: 40-60% gross margin is the operator benchmark; dropshipped wellness gear can reach 50-70% but with weaker brand defensibility (Shopify)

- Key risk: consumer-app fatigue and ad-cost inflation are squeezing DTC unit economics; FDA scrutiny on personalized-medicine claims is increasing

- Anthropological note: this is the segment whose growth is most dependent on younger consumers' continued willingness to pay for category proliferation. If Gen Z purchasing softens, this segment softens disproportionately.

The HSA / FSA reimbursement channel — a strategic differentiator

Almost no general "wellness business" article on the SERP covers this, and it is a meaningful commercial advantage for operators in the right categories.

Acupuncture, chiropractic care, and naturopathy are all reimbursable through HSA, FSA, and HRA accounts in 2025 — when performed by a licensed practitioner to treat a specific medical condition (HealthEquity FSA QME list, HSA Store — Alternative Treatments). Most plan administrators require a Letter of Medical Necessity (LMN) from a physician or licensed provider documenting the condition being treated. Cash-based general-wellness services without a documented condition are not eligible (Forma 2025 guide).

What this means for operators: a licensed acupuncturist or naturopathic physician who is willing to do the clinical documentation work — diagnose, document, prescribe, refer — unlocks a covered-care patient segment that a cash-only practitioner cannot reach. Therapy and mental-health services from licensed clinicians are widely covered without the LMN requirement, which is why the mental-wellness segment is structurally easier to bill than the holistic-modalities segment. Building a practice with reimbursement in mind from day one is meaningfully different — operationally, financially, and clinically — from building one that bolts billing on later.

Cooling segments — what to enter cautiously

The wellness industry is not uniformly rising. Three signals operators planning entry should know:

Workplace wellness contracted 1.5 percent from 2023 to 2024 — the only segment among GWI's eleven to decline (GWI 2025 Monitor). Employers are cutting generic step-counter and stress-app programs that produced no measurable outcomes. Mental-health spending within the corporate channel is still rising sharply (see segment 4), but operators building generic corporate-wellness offerings face structural headwinds.

Consumer meditation-app downloads have collapsed: Calm -61%, Headspace -74% between 2018 and 2024 (appinventiv 2025). Revenue per remaining user is still strong, but the user base is shrinking. Entering this segment as a thirteenth consumer meditation app is not a good plan.

Search demand on "holistic health" has declined approximately 41 percent year over year, and the broader "wellness industry" search has cooled at a similar rate. The audience is not gone — it is more buyer-serious, more clinically oriented, and less impressed by the pandemic-era wellness marketing language that dominated the category through the early 2020s. Operators writing copy in the tone that sounded fresh at the peak of the wellness boom are losing to operators who write like clinicians.

A closing question

The seven business models above are real economic opportunities. The numbers — $441B in mental wellness, $86B in fitness tech, 14.9 percent forward CAGR in wellness apps, $147B in personalized medicine — are not marketing. The Global Wellness Institute is the most rigorous source on the category, and they are not given to overstatement.

But the question I want to leave any operator considering entry with is one my style of work always returns to: who carries the practice, and who profits from it? A meditation app at $7.7M monthly revenue does not, on its own, do the eight years of teacher training the tradition behind the app required. A wellness retreat priced at $850 a day does not, on its own, repair the community where the bodywork tradition it draws from originated.

Some operators close that gap thoughtfully — by paying lineage teachers, by crediting source traditions in print, by reinvesting in originating communities, by refusing to sell what they have not earned the right to sell. Some do not. The wellness industry's $6.8 trillion is going to be spent either way. Where you stand inside that flow — as someone who carries a practice forward or someone who extracts its surface — is a question the financial spreadsheet alone will not answer.

The data is solid, the trajectory is up, and the opportunities are real. The translation work — between practice and product, between community and consumer — is the part that does not show up in the CAGR.

Frequently Asked Questions

The global wellness economy reached $6.8 trillion in 2024 and is forecast to hit $9.8 trillion by 2029, growing at 7.6% annually, according to the Global Wellness Institute's 2025 Monitor. Personal care and beauty (19% share), exercise (16%), and nutrition and weight loss (16%) are the largest segments by revenue.

Startup costs depend on the business model. Digital businesses (online coaching, courses, content) typically run $100-$2,000. Product brands (supplements, skincare, wellness goods) range from $3,000 to $60,000 or more depending on private-label vs custom formulation. Boutique studios, clinics, and wellness centers run $20,000-$150,000, with full retreat centers exceeding $50,000+. Most operators target 40-60% gross margins.

Yes — all three are reimbursable through HSA, FSA, and HRA accounts when performed by a licensed practitioner to treat a specific medical condition. Most administrators require a Letter of Medical Necessity (LMN) from a physician or licensed provider. Cash-based 'general wellness' services without a documented condition are not eligible. Therapy and mental-health services from licensed clinicians are more broadly covered.

Employers see an average return of $3.27 in healthcare savings plus $2.73 in reduced absenteeism per $1 invested, and 95% of companies that measure their wellness ROI report positive returns. Mental health programs specifically yield approximately $4 returned per $1 invested. In 2025, 86% of insurance brokers reported clients increasing mental-health investment, the sixth consecutive year mental health led the priority list.

Wellness real estate leads at 19.5% annual growth (2019-2024), followed by spas (+14.6%), wellness tourism (+13.8%), mental wellness (+12.4%), and thermal/mineral springs (+11.1%). Wellness apps as a digital sub-category are forecast at 14.9% CAGR to $26.19B by 2030. Workplace wellness is the only segment in decline (-1.5%), although employer mental-health spending is rising sharply within it.

Health and wellness coaching has the lowest entry cost ($100-$2,000 for a digital practice plus $300-$5,000 for a credential), the lowest regulatory burden in most US states, and an unusually open ranking opportunity online — 'wellness coaching business' has a Keyword Difficulty of 2 in major SEO databases. It is also the most crowded category by competitor count, so a credible content footprint and a specific clinical or training credential are the differentiators.

Yes, but unevenly. Consumer meditation apps have contracted sharply (Calm downloads -61%, Headspace -74% between 2018-2024), workplace wellness has shrunk 1.5%, and search demand for 'holistic health' has declined roughly 41% year over year. At the same time, mental wellness, wellness real estate, wellness apps, personalized medicine, and wellness tourism are all growing in the 9-15% annual range. The audience is more buyer-serious and clinically oriented than during the 2020-2021 peak.

Check Out These Related Articles

Financial Fitness: Exploring the Intersection of Wealth and Well-Being

Emotional Well-Being: Consumer Priorities and Influential Factors

The Economics of Integrative Medicine: Balancing Health Outcomes with Financial Considerations